Follow us

Follow us Follow us

Follow usObjective and methodology of the survey

The BalticVC media team conducted its second study of the Baltic startup ecosystem, the Baltic Startup Survey. The partner of the survey became "Yellow Rocks!" The study was conducted in the form of a survey of startup founders from Lithuania, Latvia, and Estonia.

The main goal of the Baltic Startup Survey is to describe the current state and development vector of the startup industry in the Baltic countries, identify changes that have taken place over the past year among local innovative companies, and study aspects of their activities such as team and business development, sales, and investments. The main subjects of the study were the startups themselves and their founders, their socio-demographic status, professional and entrepreneurial experience.

We invited more than 300 founders to participate, 119 of whom completed the questionnaire. We did not divide the survey results by country if they corresponded to the overall Baltic results. We only show last year's results in the graphs if they differ significantly from this year's results.

Baltic startup founder’s profile

- 41 y.o.

- university degree

- entrepreneur with experience in managing his own business

Over the past year, the founder of a Baltic startup has “aged”. The average age of a founder is now 41, compared to 39 a year earlier. Our youngest respondent is 19, and the oldest is 60. In Estonia and Lithuania, the average age of founders is even higher, at 42. In Latvia, it is 39.

The sharp increase in the share of founders aged 36-45 from 45% to 58% (by 13 percentage points) is noteworthy. The main driver of change was most likely a natural cohort shift (young founders aged and moved into the next age group). We are probably seeing a steady trend towards the “maturation” of the startup ecosystem in the Baltic region.

RECOMMENDED FOR YOU

Resilience Media Raises Seed Funding To Build The Voice Of NATO’s Defence Tech Ecosystem

Kailee Rainse

Aug 6, 2025

[Funding alert] Zurich-based CarbonPool Raises €11.2 Million in Funding

Team SR

Jan 29, 2024

Compared to last year, the number of founders with previous entrepreneurial experience decreased by 12%. At the same time, the other categories remained virtually unchanged.

Startup profile

- Founded 5 years ago or less

- Team of 2-5 employees

- At the pre-seed stage

The average startup in the Baltic states is 1-5 years old.

Startups with a single founder are not yet very common in the Baltic states. Only 5% of startups belong to this type. Most Baltic startup teams are small, consisting of 2-5 employees (38%) with just 10% having 31 or more associates.

Almost half of startups are at pre-seed stage (42%), 28% of companies are at seed stage, and 16% of companies are at early growth stage.

To classify startups, we asked founders to name the industry in which they operate. As in the previous year, startups most often mentioned Fintech or related industries such as Regtech and Insurtech. Education-related companies ranked second in popularity, followed by startups involved in BioTech, HealthTech, and MedTech. Artificial intelligence ranked only fourth in terms of frequency of mentions by startup founders.

Compared with last year's survey results, we see a significant decrease in the percentage of startups that identify themselves as B2B companies (from 82% to 59%). We believe that the analysis has revealed a unique trend. The core of “pure” B2B startups has remained unchanged (37% in both 2024 and 2025), while the overall mention of the B2B model has declined sharply. Since the survey methodology has not changed and the shares of other models (B2C, B2G, B2E) have remained virtually unchanged, we conclude that there has been a massive refocusing of startups.

A significant number of teams that previously positioned themselves as hybrid (B2B+X) worked throughout the year to simplify and focus their business model, abandoning the B2B direction as non-core or too resource-intensive. The B2B segment did not shrink, but rather cleared itself of non-core players, which in the long term may indicate its healthy concentration and ecosystem maturity.

The shakeout in the B2B segment could have been caused by several reasons. For example, due to economic uncertainty, startups may have abandoned this direction in favor of simpler ones. In addition, investors may have recommended that teams “focus on one thing” and choose the most promising model. And this choice often did not fall on B2B.

Startup industry scene

More than half of Baltic tech entrepreneurs (53%) say that, overall, the situation in their business has changed for the better over the past year. 32% of respondents said that the situation in the industry has not changed, while 15% of founders felt that it had deteriorated. At the same time, 31% of respondents said that their business was close to closing in 2024.

Looking at the results by country, 50% of start-ups in Estonia felt that the situation had improved, 30% felt no change, and 20% felt that market conditions had deteriorated. At the same time, every fourth Estonian startups was on the verge of closing in 2024.

Latvia shows similar figures: 56% of respondents believe that the situation in the industry has changed for the better. 30% did not notice any changes, and 14% felt that the market situation had deteriorated. 36% of startups were on the verge of closing in 2024.

Only 7% of Lithuanian start-ups felt that the market had deteriorated. 56% of respondents said that the situation in their industry had improved. 37% said that the situation had not changed. 31% of start-ups in Lithuania admitted that their business was close to shutdown last year.

Sales

“The question about revenue dynamics makes it possible to understand how "alive" Baltic startups remain even at the earliest stages. Despite the fact that 42% of companies are still on pre-seed, 90% of respondents have had their revenue grow over the past six months. At the same time, for 43% of startups, the average growth is only 1-10% per month - this is not a story of hypergrowth, but neat, organic growth from small bases. From an investor's point of view, this is a signal of a more pragmatic market: teams test hypotheses, pay attention to efficiency and do not burn money for beautiful graphs, but at the same time they already know how to convert a product into real money”.

Sergei Bogdanov, Managing Partner at Yellow Rocks!

In terms of sales geography, most Baltic startups continue to focus on the local market (66%) and the EU market (78%). The US and Canadian markets account for 24%. Sixteen percent of projects have entered the MENA market, and 15% operate in Latin America.

For most Baltic startups (46%), the Baltic countries account for the majority of their revenue. At the same time, 36% of companies, on the contrary, generate 0-25% of their sales revenue in the local market. Thus, last year's trend of dividing Baltic startups into two almost equal parts, one focused on the local market and the other on the global market, remains in force. Lithuanian startups remain the most internationally oriented of the three countries.

Funding. Startup’s investment profile

Baltic entrepreneurs tend to believe that investors have become more cautious - this is the opinion of 60% of respondents. 24% of those surveyed did not notice any changes in investor behavior, while another 16% noted increased interest in startups.

If we rank the responses by country, Latvian start-ups are the most pessimistic on this issue, with 54% feeling a decline in investor interest.

56% of founders launched their companies using their own funds. Another 11% used grants.

One in four startups continues to grow thanks to founders' capital (26%). Other important sources of startup funding currently include sales revenue (also 26%) and venture capital funds (19%).

Baltic startups founded at the expense of the owners' capital, for the most part, either continue to live on their own money (43%), provide themselves with sales revenue (20%) or have already managed to attract money from venture funds (15%).

The startups that attracted money from the accelerator at the start turned out to be the least sales-oriented. Only 14% of them now live on the proceeds from sales. More than half (57%) were able to attract grants.

The number of Baltic startups with external investors is 57%. Latvia has the least of these (only 40%).

57% of the investments received by Baltic startups can be classified as pre-sowing, and another 34% as seed. The last round received is classified as Series A or B by 9% of companies.

Last year, the majority of surveyed Baltic startups raised up to 300K euros and from 300K to 1M euros (41% each), but this year the share of startups that raised from 300K to 1M euros fell to 24%.

Most likely, this can be explained by the fact that the Baltic startup financing market has become more polarized. Investors have concentrated their capital on two poles: small seed investments to test hypotheses and large rounds to scale proven models. The classic "expansion" round of €300k - €1M turned out to be the biggest loser, as investors began to consider it too risky for their potential returns. This segment ended up in the "valley of death". To investors, such companies no longer seem as promising as the early ones, but they are not yet mature enough for large-scale investments. The trend is developing in such a way that "the strongest or the cheapest survive".

We see an ecosystem that is maturing and going through a stress test at the same time. The founders have become older and more experienced, the B2B segment has been cleared of "random" players, and revenue and grants are beginning to play a significant role in financing, while investors are generally more cautious and polarize the market of rounds between very small checks and large transactions. Against this background, it is those teams that are particularly valuable, which, even in a complex macro environment, show moderate but stable growth and are able to build a business with an understandable economy — such companies, in my opinion, will be most interesting to investors in the coming years.

Sergei Bogdanov, Managing Partner at Yellow Rocks!

BalticVC would like to thank Startup House Riga, EdTech Estonia, Startin.lv, Beamline accelerator, Digital Accelerator of Latvia, BSV Ventures, Health Founders Accelerator, Startup Lithuania and many others who helped us conduct this survey.

Recommended Stories for You

Kailee Rainse Apr 29, 2025

Kailee Rainse Jan 22, 2026

Akribion Therapeutics funding news – Germany-based Akribion Therapeutics Secures €8Million in Funding

Kailee Rainse Feb 4, 2025

Kailee Rainse Feb 18, 2026

Trending Stories

Chipiron Funding News- France-based Chipiron raises €14.9M

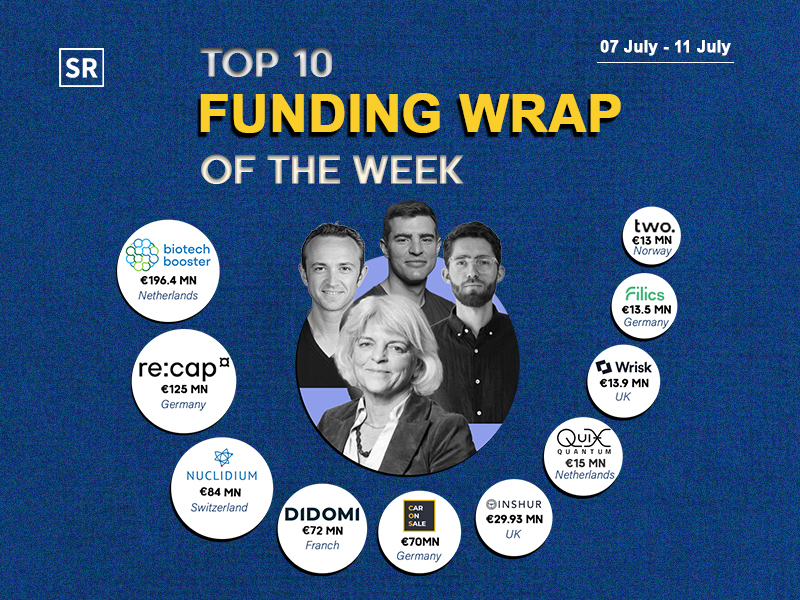

Top Funding Wrap of the Week – July 07 – July 11 2025

[Funding alert] UK-based Cambridge Mechatronics Secures €37 Million in Funding

Alpine Eagle funding news – Munich-based Alpine Eagle Raises €10.25Million in Seed Funding

ASTRA Therapeutics Secures €8.3M To Advance Precision Parasiticides For Animal Health

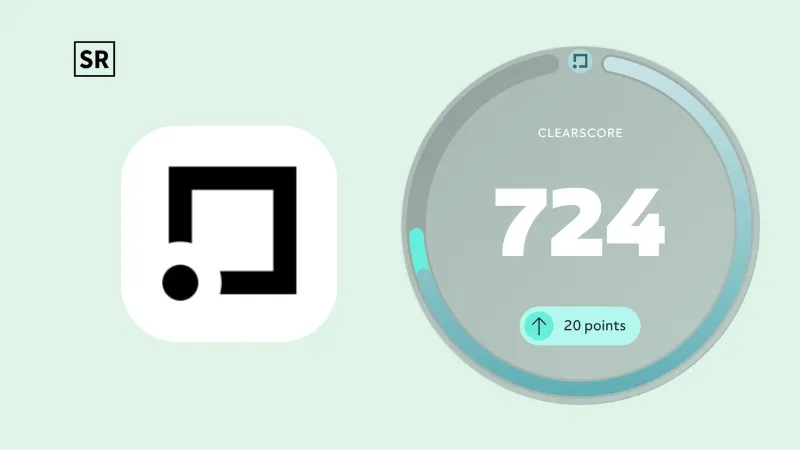

ClearScore funding news – Credit Score Service Fintech ClearScore Raises £30Million in Debt Funding

Cloud Capital Secures $7.7M Funding to Put CFOs Back in Control of Cloud Spend

Your.World funding news – Amsterdam-based IT group Your.World Raises €800Million in Funding